Announcement on 30 April, 2024

Tesla Is Paving The Way For Growth After A Negative Q1 2024 Cycle

- Tesla reported a 9% drop in first-quarter revenue, the biggest decline since 2012, due to demand reduction from economic pressures, as well as impacted by price cuts. Tesla's net income dropped 55% to $1.13B. While Tesla is in a downcycle, I expect the shake-up to be positive for the future growth of the company.

- In the investor call, Tesla noted that it’s continuing to train AI infrastructure using more than 35K H100 NVIDIA GPUs, and is in talks with a major automaker to start licensing FSD. Musk compared the current state of automobiles with the days of manual elevator operation, noting that “today we just press a button on the elevator and don’t think about it”, which is what the CEO aims to accomplish with FSD EVs.

- Tesla recently underwent a restructuring, with two executives resigning and the company reducing its global workforce by more than 10%. This is expected to create annual savings of $1B and help optimize the company.

- A notable risk factor, mentioned in the presentation and reiterated by Musk, is that many carmakers are prioritizing hybrid vehicles over EVs. The advantage of hybrids is that they can use interchangeable fuel cells and gas in order to instantly fuel vehicles, while Charging EVs takes time and relies on grid infrastructure stability which was never constructed for the EV-implied demand. I cover this risk factor in my narrative, and will continue to monitor how the industry develops over time.

- During the Q&A, the CEO was asked, excluding all FSD features, how long will it take for competitors (chinese) to copy Tesla’s EVs? To which Musk responded that the right way to value Tesla is as an AI-robotics company, instead of a carmaker. This is a point worth considering, as Tesla moves from luxury to affordable EVs, its profits will have to be made by software and add-on services. Tesla’s approach seems to be shifting to cheap EVs, with upselling opportunities tailored to customer’s budgets.

- Tesla is ramping up the production of the cybertruck, and is in early phases with the semi with the construction of the plant in Reno. The combination of FSD with a Semi fleet is one of the larger value propositions from Tesla, since a realization of FSD would decrease the number of needed consumer vehicles, while freight is not as interchangeable.

- Musk commented that Optimus is being tested in the lab, and we may get some worthy developments by the end of 2025. I maintain that it is too early to value Optimus, as the competitive landscape will change in two years. However, Musk is right that they will be able to use some of the FSD technology for training a humanoid in perception and motion.

- Tesla re-unveiled a mockup for the robotaxi app, however critics were right to point out (comments) that Musk had used this as a prop back in 2019, which isn’t by itself wrong, but may highlight the company’s need to push positive stories during a negative quarter.

- Analysts that point out Tesla’s high aspirations may forget that Musk’s wild futuristic propositions is a crucial part of the job of a CEO i.e. throw out ideas and monitor the market’s and investors’ interest in deciding what to pursue. However, in my narrative I need to reconcile the possible with the probable, and as of this quarter I maintain that a 2029 forward value of $870B captures most of Tesla’s risk & potential.

Key Takeaways

- Tesla’s auto market share will grow but less than investors expect

- The semi will contribute $17.5B if its value proposition matches that of ICE trucks

- Energy revenues will reach $16.7B in 2028 as industry tailwinds support continued growth

- If FSD wins, it’s at risk of being shared by government safety mandates

- PE will re-rate lower in long term to be similar to current auto peers

- Business has great growth prospects, but even they don’t justify current price

Catalysts

Tesla’s TAM and Market Share Has Limitations

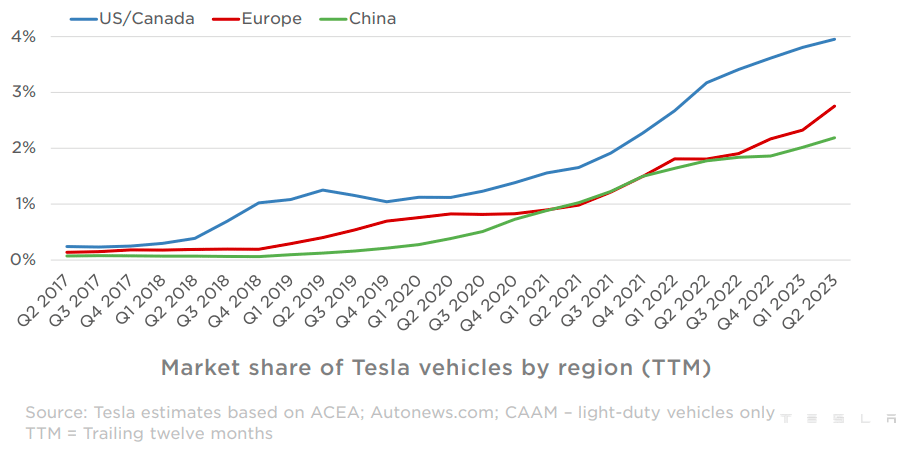

In the last 4 quarters ending Q2’23, Tesla has delivered 1,638,123 vehicles. Approximately 46.8% of total sales are made in the U.S. and we can use this as a basis to estimate the number of vehicles sold in the U.S., which comes out to 766,478. Looking at the market side, the seasonally adjusted annual unit sales in the U.S. is 15,735,000 autos and light trucks (SUVs). This means that Tesla has around a 4.9% market share in the United States - fairly consistent with the company’s presentation (p. 7). Looking at the company’s chart, we see that Tesla has estimated around a 4% market share in the U.S. & Canada, 2.8% in Europe, and 2.2% in China.

Company Presentation: Market Share of Tesla Vehicles by Region in the Last 12 Months

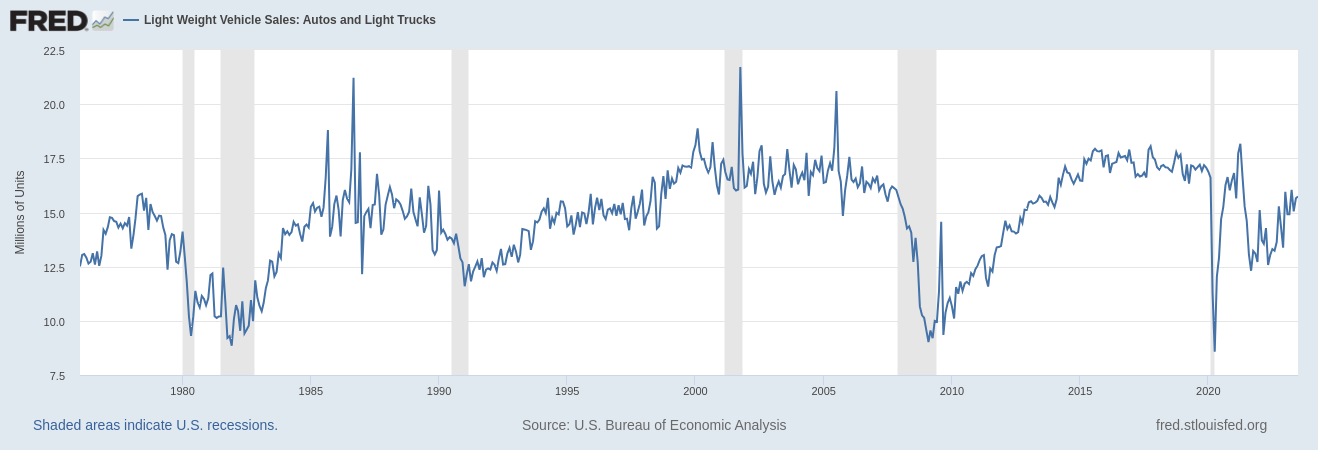

Market Share Gains of U.S. Light Vehicle Likely Lower than Investors Expect

The light vehicle market is closer to a saturated cyclical market, rather than a growing market. However, the rise of mobility platforms like Uber and Lyft, may decrease the need for auto ownership in a small portion of the population, further compressing the future addressable market. Note, even though autonomous driving technology has the potential to increase vehicle utilization rates, I assume that this will be mostly taken up by ride hailing companies, and everyday consumers will be reluctant to “rent out” their vehicle to strangers.

FRED: Light Weight Vehicle Sales in the U.S.

This indicates that one point of possible hindrance is Tesla’s position in a saturated market, and their main growth approach is capturing market share from competitors. With the current stock price, the market seems to expect that Tesla gains more than 21.5% of the light-auto market. However, below I explore why gaining more than 15% may be difficult for the company.

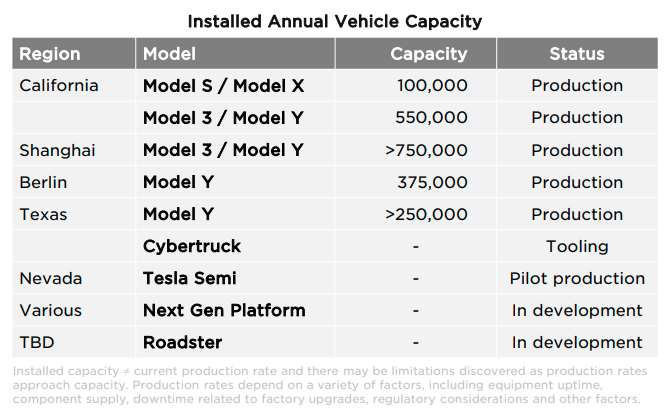

Tesla’s Production Capacity Will Increase Dramatically

An overprovisioning of capacity expansion CapEx will be taxing for investors in this scenario, which is why it may be better for the company to be slower on capacity expansion. Currently, Tesla has about a 2 million total vehicle production capacity, indicating that the company can grow revenues by 24% (because it currently builds 1.63m vehicles). After that, it will need to increase capacity, pricing or focus on other revenue streams.

Company Presentation: Annual Vehicle Production Capacity

The first new capacity upgrade to come online will be the cybertruck, which is expected to make its first deliveries by the end of 2023 (p. 10). It is estimated that there are close to 2 million non-binding cybertruck reservations, and Tesla is initially planning a capacity expansion of 375k units in Giga Texas, with a possible extension of production to Mexico.

This indicates a near-term expected increase in production capacity to a total of 2.4 million units, paving the way to a 46% total revenue increase at full production capacity.

By applying a stable geo-segment portion of 48% sales for the U.S., we can estimate that the light vehicle market share for Tesla is on its way to reach around 7.3% by 2033.

As Tesla has delivered 1.6 million vehicles, and is increasing its production capacity to 2.4 million, I estimate that the growth in sales in the next 4 years will reflect the total capacity, and revenues will increase by 50% to $141B or about 13% per year.

Despite the high demand, I project that the company will be the most successful in its home market of the U.S, experience stagnant success in Europe on account of established competitors, and under-perform in China because of the risk in an increase of protectionist policies.

Given the set groundwork, I expect the company to reach a 15% U.S. market share, 8% in Europe and 7% in China. The company is scaling rapidly, so I expect it to reach its saturation point in the next 10 years. This implies a top line growth of 275% in the U.S. (14.13% CAGR), 186% in Europe (11% CAGR), and 218% in China (12.3% CAGR).

Assuming that the distribution or revenues stays roughly the same for each geo-region, based on my target market share this would yield revenues of:

- Base: total revenue ex energy in the last 12 months = $88.5B

- Legend: region, geo-segment revenue % * auto segment revenue % * growth = est. revenue

- USA (46.8% * 94.2%) 41.4B * 3.75 = $155.2B

- Europe (22% * 94.2%) 19.5 * 2.86 = $55.7B

- China (31.2% * 94.2%) 27.6 * 3.18 = $88B

This results in total 2033 light vehicle revenues of $300B, up by 240% from the last 12-months, representing a 13% CAGR.

The Good and The Bad From Tesla’s Self Driving Technology

The development of autonomous driving technology has the potential to transform a portion of the mobility industry. As we get closer to self-driving vehicles, the need for drivers will decrease, enabled by short-distance autonomous ride hailing. While self-driving vehicles are still unsafe, they may reach a point where they are much safer than human-driven vehicles, which would reduce their insurance premium and make them more attractive to customers.

Part of the issue is that the safety liability with human-driven vehicles is decentralized to each individual driver, while self-driving manufacturers like Tesla may bear most of the liability since the driving relies on their technology. Should we see a shared liability between the vehicle owner and manufacturer, I believe that the adoption pace of self-driving vehicles will increase.

Besides auto ownership, the two key segments that are likely to be impacted by autonomous driving are consumer mobility and freight transport.

Mobility - A Key Revenue Growth Driver

Looking at our Big Trends analysis, I note that the cost of ride-hailing with autonomous vehicles can drop from the current $2 per mile to as low as $0.25 per mile, an 8x reduction. The potential cost reduction is a key value proposition for ride-hailing companies, as well as a factor that can impact future consumer preferences.

It seems that this will lead to a larger uptake of partly autonomous vehicles, but at the same time will reduce the need for vehicle ownership in favor of shared mobility. For Tesla, this means that the technology will reduce their TAM as customers start adopting mobility solutions instead of owning vehicles.

On the other hand, proponents of Tesla may argue that the developed self-driving software will increase margins and make up for the potential loss in revenue. However, while Tesla will be able to license its software, it is highly unlikely that they will manage to keep it at a high margin level, especially when governments step-in and decide to standardize self-driving technology across manufacturers.

In my opinion, there is no scenario where an auto manufacturer has an accident rate of say 0.05% and another has 0.01%, the one with the superior technology will be forced to license out the software to peers. For this reason, I view Tesla's self-driving technology akin to developing a premium medicine - high-margin for a period of time, but then turned “generic” by regulators, with margins that converge on the cost of capital.

Freight Transportation - Another Big Opportunity, If They Can Win

One of the rare ways in which Tesla can surpass the growth limits is to diversify horizontally and expand into freight trucking.

Unlike mobility, Tesla is leading the development in this avenue and has the potential to emerge as a winner, especially if their “Tesla Semi”, can manage to produce sufficient mileage and reduce the costs of trucking companies.

In the U.S., trucks average around 500 miles per day (1, 2) which is why it is important for Tesla to reach that mileage capacity, else risk being less versatile in its value proposition. An autonomous freight truck is attractive primarily because of the reduction of labor costs, and costs associated with human error, which show up as high insurance premiums, and error-induced maintenance costs.

The estimated cost reductions for autonomous transport come down to $0.06 per mile, from today’s $1.6 per mile. This is a large potential target, consisting of around 50 publicly listed companies in the U.S. Transportation industry with close to $214B in annual revenue.

On the labor side, in the U.S. there are about 5.6 million employees engaged in some form of ground transport, representing about 3.6% of the 156 million U.S. nonfarm employees. Transportation occupations have a median annual salary between $44.4K (1) and $62.4K (2), with a midpoint at $53.4K and 5.6 million workers.

The automatization of this industry has the potential to reduce costs up to $300B in value. Naturally, not all of the industry is suitable for automation, and in the next 10 years I expect that 40% of it is a realistic automation candidate, reflecting a $120B potential in cost reductions.

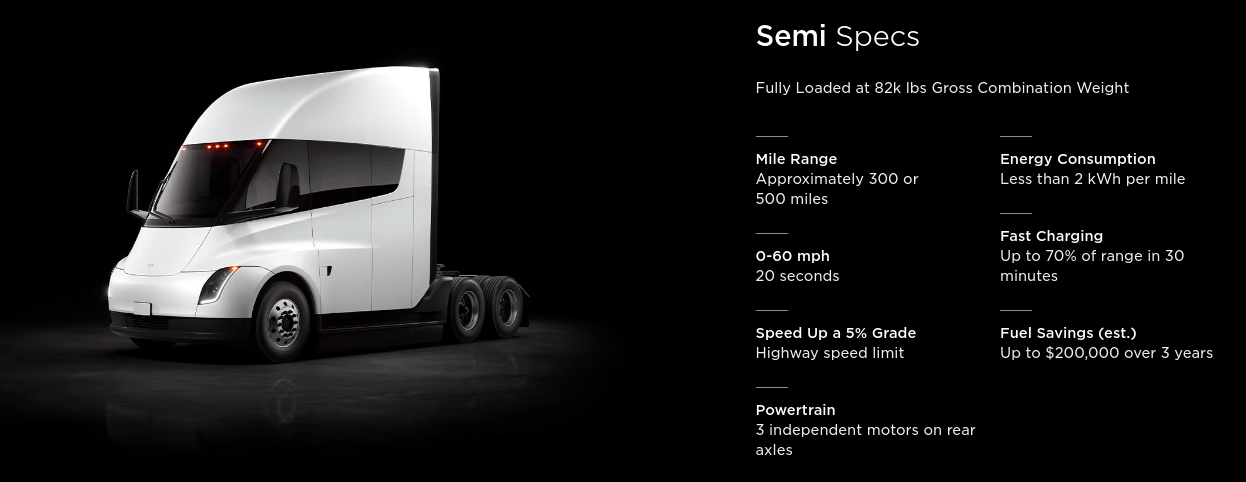

Out of 13 million registered trucks in the U.S. there are approximately 3 million semi-trucks, which is the vehicle type that Tesla is pushing. The semi is a large truck used for transporting heavy cargo on long routes. The current price estimates for the semi are around $250K, roughly twice that of their internal combustion engine (ICE) counterparts.

Tesla is gearing up for a production capacity of 50K semis per year, and assuming it converts 100% of them in sales, it would make $12.5B in annual sales in 2025 when volume production is expected to start per Musk.

This refers to the North American market, after which Tesla aims to expand, but given that the US is still a primary market for Tesla, I consider the 50k unit projection a balanced average of what we can expect in the next few years. This implies that Tesla would gain about 1.7% of the market share. However, the lifespan of the ICE counterparts is about 15 years, so Tesla can make it to around 10% of market share in 10 years, as customers don’t need to buy new semis every year.

Bottlenecks to the EV Transition - Generating Enough Energy To Meet Demand

In their impact report Tesla paints an optimistic scenario (p. 71) “When fully loaded, the Tesla Semi should be able to achieve over 500 miles of range, achieved through aerodynamics and highly efficient motors. This truck will be able to reach an efficiency of over 0.5 miles per kWh.” Along the website, both 300 miles and 500 miles are used as estimates for the Tesla semi mileage capacity, which is quite the difference. Semis would require a special charger, that would allow them to charge up 70% in 30 minutes.

In order for this business to pick up, the value proposition must be clear and self-evident to customers.

This includes delivering on the promises of energy savings as well as headcount savings. Competitors may decide to enact penalties to switching the fleet manufacturer, so Tesla will need to be able to reliably overcome this in the long-term, which is why gaining market share may be initially slower for the company.

Company Website: Tesla Semi Key Specifications

Grid electricity will have challenges to support charging EVs, which is why some form of decentralized solution is necessary. This is likely why it makes business sense for Musk to integrate battery and solar solutions as supplements to Teslas.

However, this solution may not be enough, especially for large semi trucks. It is estimated that charging a semi truck with a fast charger is equivalent to providing 1500 homes with electricity. One charging station will need the power capacity of its own substation.

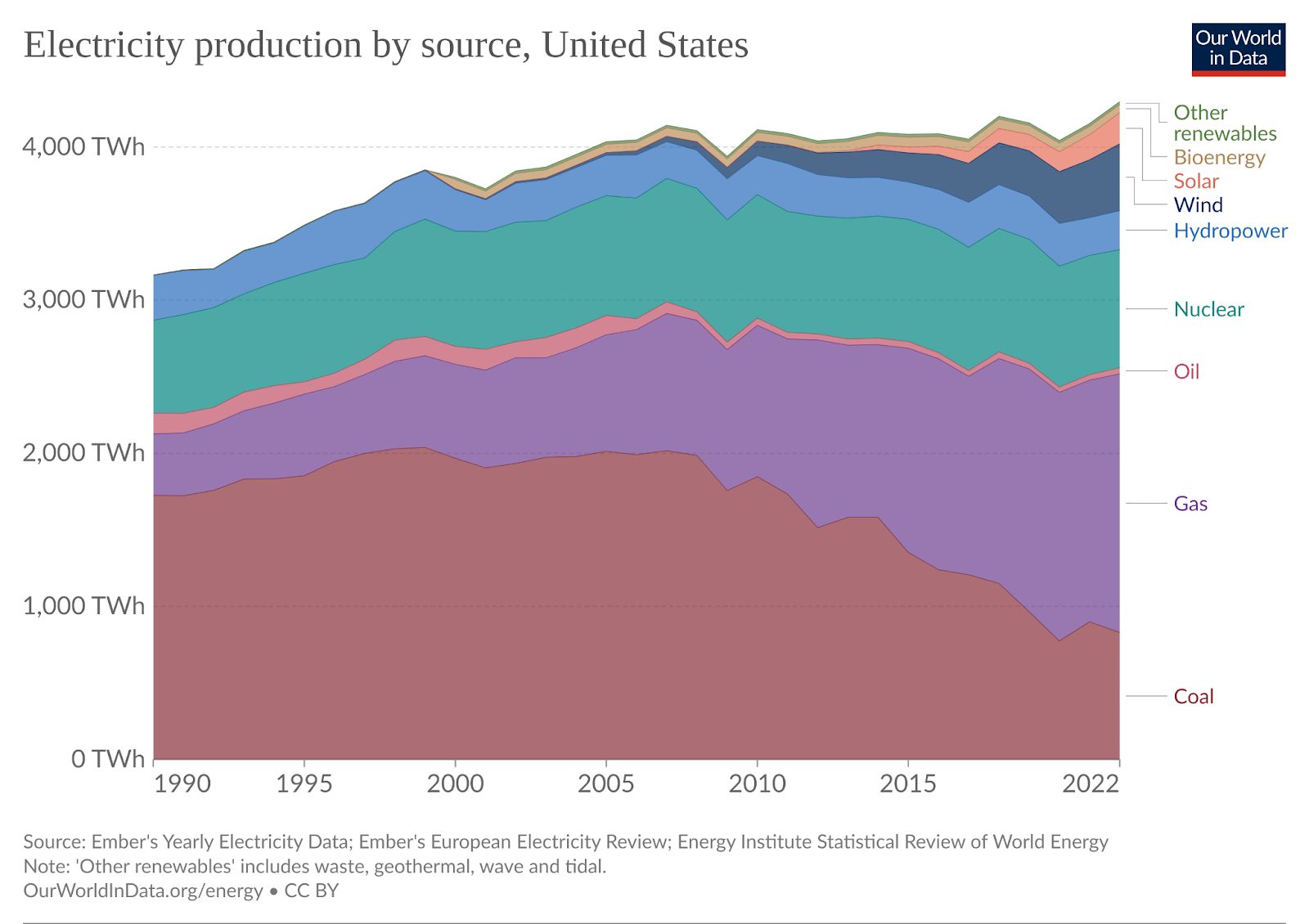

Given our analysis thus far, we can estimate an average daily mileage for a semi truck of 500 mi, and average time in operation of 300 days per year. With a 2 kWh per mile spend, it would take 300 MWh to power one Tesla Semi. In a scenario where all registered 3 million semi trucks switched to electric energy, it would take 900 TWh (300MWh * 3,000,000) per year to power the fleet in the US alone, taking up 21% of the current 4,300 TWh electricity production.

Our World in Data: U.S. Electricity Production by Source

Additionally, transitioning to EVs may increase power demands by 2x in highly populated areas and we may not yet have the infrastructure needed to sustain and deliver the electric load.

This is why the sheer electricity demand that these EV autos and trucks would produce makes this proposition unfeasible in the term of 10 years in which we are valuing Tesla. Instead, we can lower our projections and estimate that the US would be able to sustain a 20% transition to EV semi trucks, of which the bulk of the market share would be allocated to Tesla.

In the U.S. this comes out to selling a cumulative 170K units at a $250K price up to the first half of 2028 - $12.5B in annual revenue. After that Tesla would sell an annual 70k units after that, leading to a total of 520K units sold ($17.5B p.a.) in the next 10 years, converging on a 17% U.S. semi truck market share.

This means that in 7 out of 15 years (average semi depreciation time) Tesla will be gaining market share, and in the other half it will be selling to maintain its market share.

An embedded assumption here is that the market adopts decentralized electricity generation solutions for consumers that reduce the power grid load in charging stations, as well as increasing electricity generation by 3.6% in the U.S..

Should the rise in electricity demand be gradual, then we may find that initiatives such as the Inflation Reduction Act of 2022 (which allocates $369 billion to renewables), will help drive a plausible transition.

Long Haul Freight

Estimating an increase in Tesla’s semi market share beyond 20% may be unrealistic for 2 reasons:

- The natural competitive environment will divide purchasing by brands and a portion of truckers will opt to stick to ICE trucks.

- Hydrogen powered trucks may be a more appropriate alternative (1, 2) for trips longer than 500 miles, as they have faster charge times and can travel further on a single charge. Their drawbacks include possible safety concerns, a lack in charging infrastructure and storage.

Energy and Storage - Another Key Revenue Driver, Supported by Tailwinds

Tesla’s energy and storage business commands a respectable 5.8% of total revenues. Energy generation and storage sales jumped to $1.509B by 74% YoY. This is a high increase pointing to an increased uptake in the market for these products.

However the trend is flat Q-Q, indicating that the uptake from a year ago may be stagnating.

Most of the rise is attributable to the sales of energy storage solutions - 3653 MWh in Q2’23, vs the declining solar solutions of 66 MWh in the same period. The company also employs 5265 supercharger stations with 48K supercharger connectors, both up 33% YoY.

It seems that Tesla is scaling its charging infrastructure and starting to increase the foundation for a higher use of its vehicles.

As governments transition to clean energy solutions, we may see the increased subsidization of this industry. Both Europe and the U.S. are investing heavily in its infrastructure, with the most notable programs including:

- Infrastructure Investment and Jobs Act (US): $1.2T planned investment which includes EVs and an electric grid renewal.

- Climate and Energy Provisions of the Inflation Reduction Act of 2022 (US): With a $737B allocated to support projects across electric vehicle (EV) charging, renewables, power infrastructure and climate resilience.

- Recovery plan for Europe with an estimated investment budget of €2.018T.

Tesla and other peers in the renewable energy space are set to benefit from these tailwinds, which is why the energy branch may be a key growth avenue in the future.

The only real bottle-neck to this growth may be processed battery raw material sourcing - as lithium carbonate demand is estimated to reach 3 million metric tons annually by 2030, while the 2021 output amounted to 540,000 metric tons (18% of the anticipated demand).

Tesla is investing to keep up with demand in refining lithium, as the refining process can also be a bottle-neck along the supply constrained mining. However, on a global scale, in order to reach these levels, the output will need to increase by 25% annually, which is my proxy for the estimated growth of Tesla’s energy and storage solutions - primarily because batteries make up 98.2% of the energy and storage business.

This means that I anticipate the energy segment to grow to $16.7B by 2028 and $37B in 2033.

Interestingly, the estimated global lithium resources currently stand at 98 million tons. Barring new large deposit discoveries, and considering the estimated annual demand of 3 million tons after 2030, we may start seeing supply gaps after 2062 - a best case scenario analysis puts this limit year around 2100.

With that in mind, it seems that hydrogen fuel EVs may be a potential future pivot for Tesla, since it is a renewable source of energy storage e.g. via water electrolysis.

Loose Ends - Thoughts on FSD and Optimus

Full Self Driving Will Likely Increase Revenues, But Not Margins

I expect Tesla to sufficiently develop its full self-driving technology, and feel that this will contribute to the rise in gross margins. There are 2 key issues with extrapolating high value generation with this technology:

- Competitors like Waymo may create a service that is on par or superior to Tesla’s FSD

- Once FSD is established, governments will likely mandate the licencing of the superior technology to all auto manufacturers, which will even out Tesla’s competitive advantage

The highest contribution to FSD will be the initial push in the rise in market share for Tesla, which is why I’m comfortable with assigning premium future revenues, but cannot extrapolate too much on the margins.

Optimus Won’t Contribute To Profits For A Long Time

Tesla’s humanoid robot is not factored-in as a revenue stream in my analysis, because even if the technology develops, it will take more than a decade before it shows up as profit to shareholders. Technological developments tend to be gradual and then rapid, however the time it takes for them to be converted to profit may be longer than expected. And until then, they typically are a cash intensive requiring lots of research and development costs and capital expenditure into PPE .

Assumptions

Auto and Semi revenue to reach 15% of market in 2033

Based on my projections, Tesla will reach revenues of $355B in 2033 consisting of $300B in auto, $17.5B in semi, and $37B from energy solutions. For the next 5 years, I project that Tesla grows revenues roughly by 15% p.a. and reaches $190B.

By consolidating the largest auto markets, we can see how much revenue is produced by the bulk of the auto industry: US $486.3B, Germany 650.1B EUR, France 100.3B EUR, United Kingdom 7.8B GBP, Japan JPY 90T, China CNY 1.1T.

Converted to USD, the total market size for the bulk of the auto industry is $2T. (US) $486.3B + (GER) $707.8B + (FR) $109.2B + (UK) $9.96B + (JP) $611.5B + (CN) $150.8B = $2,076B

Excluding energy, the projected $317.5B will give Tesla a lower bound of the global auto & truck market share of 15%. This implies that it makes as much as top peers such as Volkswagen AG with $327.6B, Toyota Motor with $267B, and Mercedes-Benz Group AG with $167B in (USD converted) revenues for the last 12 months.

Gross Margin To Increase, But Hit A Ceiling

Tesla’s gross margin was 21.5% for the last 12-month period. The gross margin declined from a high of 27.1% in the 12-months ending at Q1’22, primarily due to inflation pressures and supply chain shortages which were heightened in that period. Gross margins between 25% and 18% for a primarily (94.2% of revenues) auto company are signals of an already well scaled business structure and it may be challenging to increase the gross margins without branching off from the main segment.

I believe that the continuous R&D and gigafactory approach will yield higher gross margins in the next 10 years, but do not see them rising above 30%. This effectively constrains our future profit margins estimates, even though I expect Tesla to be significantly more successful than other auto companies.

As a company grows, it is increasingly difficult to bump up the gross profit margin, unless management undertakes specific projects with high unit economics e.g. giga-factories, or the old school off-shoring of production.

Net Profit Margins To Increase Slightly

Current TTM profit margins stand at 13%, down from a high of 15.7% in FY 2022. The company has a great balance sheet and is de-leveraging, but as it starts making money, it will see its taxes grow. The company is also employing world class engineers and various talents, along with the sales & general administrative headcount, these make up a majority (94.4%) of the company’s operating expenses.

I expect the company to keep investing in its R&D and sales force, and find that the operating expenses are just 8% of total revenues - a highly optimized structure with little room for improvement.

Because of this, I estimate that Tesla will regain its pricing power and increase net profit margins to 16% by 2025, and expect net margins to stay at roughly that level for the following few years. However, given the gross profit constraints, it will be hard for the company to further optimize and push up its net profit margins.

This means that I expect Tesla to produce net profit of $30B in 2028 and $57B by 2033.

Earnings Multiples Will Gradually Lower

In deciding what PE is appropriate for Tesla, I use a mix of consumer auto manufacturers.

The companies I picked have mature characteristics, ex RACE, and I use their average in order to derive a PE for Tesla that will be suitable when the company approaches maturity in 10 years. While RACE is a luxury auto manufacturer, Tesla is looking for broad market share. So rather than going for smaller market share with higher premiums and higher margins (like RACE), Tesla is looking for a larger market share and thus, will likely have slightly lower margins, and thus deserve a lower PE multiple than RACE.

So to get an appropriate PE for the next 5 years, I work backwards. I adjust the PEs for my target of Tesla’s future margins (16%) and calculate what would the PE be for peer companies if they had a larger margin - assuming a linear relationship.

Here are the peers I choose for Tesla:

- VOW3 has a 4% profit margin trading at 4.9x PE. Adj. PE 19.6x

- MBG has a 10% profit margin at 4.7x PE. Adj. PE 7.52x

- TM has a 7.7% profit margin at a 10.9x PE. Adj. PE 22.64x

- RACE 19.5% profit margin at a 48.8x, PE 40x, adj. for valuation PE 17.4x, Final Adj. PE 14.3x Tesla is comparable with RACE on profitability, however the fair PE for RACE may be closer to 17.4x which implies that the company may be overvalued. In order to use RACE’s PE as a comparable, we will adjust it to the estimated fair PE of 17.4x.

Note: in the calculations we are solving for what the PE would be if the peers had a margin of 16%. We use: Target margin / current margin * current PE.

This leads us to our adjusted estimate for a Tesla PE at maturity of 16x - derived from the average adjusted PE ratios from the peers above. I expect the current 62x PE to gradually converge on the 16x PE by 2033, and estimate that it will make most of the drop by year 5 in 2028, where it will converge on a 29x PE.

In my analysis, I made Tesla into the global market leader in auto manufacturing and a company with high revenue streams from its energy business and the future expansion into trucking. I am cautious on the benefits of FSD, and think that it is too early to price-in a humanoid robot.

Risks

Here are some “what if” scenarios that can have a material impact on my Tesla Narrative:

The growth mix can be different for the company

- The bulk of the high growth may happen sooner, by Tesla maintaining higher 20%+ revenue growth rates initially. However, given the market size, this may mean that the company hits a wall suddenly after the next few years and the market scrambles to re-rate.

Competitors find ways to out sell Tesla

- Currently, the product i.e. Tesla is the main selling force behind the company. However, as customers start building-in the expectations of self-driving cars and competitors start catching up, Tesla will have to employ a strong salesforce, which is a field that traditional competitors have far more experience in. A larger salesforce also necessitates higher operating expenses.

Long tail risks and opportunities

- We may find that FSD can’t quite work with neural nets alone and the technology may be a limiting factor. This will constrain self-driving cars to safe and standardized routes, but will make the service unavailable for a portion of the population that frequent lower quality routes. On the other hand, the humanoid robot (or a simplified version) may develop faster than anticipated and the company may find a massive market fit given that Tesla is one of the rare companies working on such technology.

Hydrogen wins

- Charging hydrogen fuel cells is faster, the process needs electricity but is agnostic on how that electricity is made and is abundant as opposed to the limited deposits of lithium carbonate. Peers that adopt hydrogen EVs, especially for long-haul trucks, may have a higher value proposition than Tesla.

How well do narratives help inform your perspective?