Announcement on 30 April, 2024

Tesla misses the mark with earnings, but the market doesn’t seem to care

- Nearly a week ago now, Tesla published their latest Q1 2024 earnings figures. The headline was a 10% normalised EPS miss and a 19% GAAP EPS miss. You’d think this would have been mayhem for the share price, right? Well, not exactly. Over the last 5 days, the share price is up 35%!

- Tesla’s latest production and shipping figures weren’t anything to excite investors, with the 433,371 cars produced and the 386,810 delivered both coming in lower than the previous quarter and from the same quarter a year ago. Tesla partially attributes the decline in volumes to the early phase of the production ramp of the updated Model 3 at their Fremont factory and factory shutdowns resulting from shipping diversions caused by the Red Sea conflict and an arson attack at Gigafactory Berlin. This goes some ways to explaining some of the declines, but the reality is that the current economic situation doesn’t really lend itself to explosive growth in the automotive industry. As acknowledged in a previous update, the recent declines don’t really support my narrative, but I don’t think they’re severe enough to invalidate my narrative either. I shall hold my assumptions steady.

- More enthusiastically, Tesla reported it deployed 4,053 MWh of energy storage products in Q1, the highest quarterly deployment yet. While all other segments of the business were down, Energy Storage saw a 7% increase YoY in terms of revenue. While this does partially support my narrative that the Energy Storage business will be the strongest performing segment, it’s perhaps growing at the rate I anticipated. Mike Snyder, the Senior Director of the Megapack product, addressed a question in the latest earnings call about the Megapack, indicating that the ramp up to 40GWH of production at the Lathrop factory was proceeding as planned, which should help sales of the Megapack in some respect, but I will continue to monitor this closely as I believe I may have to downgrade my assumptions due to the longer sales cycle of the product potentially limiting upwards growth.

- Interestingly, there was no mention of the Dojo Super computer in the Earnings Call or the Earnings Release. That’s not to say I think anything has materially changed, but perhaps the process of acquiring the hardware and training the AI is a trickier process than what Tesla initially envisioned. The last mention of Dojo publicly in the Q4 2023 earnings seems to indicate that this could be the case.

Tesla’s deal to use mapping data from Chinese web search company Baidu is a big step forward for FSD

- Elon’s recent trip to China has seemingly caught the attention of Tesla investors (potentially helping them to forget Tesla’s weaker earnings report). His trip seemed to be a fruitful one, with Tesla inking a deal with Baidu, the main web search site in China. Baidu has agreed to provide mapping and navigation functions to help Tesla operate its full-self driving (FSD) technology in China.

- This is a big move for Tesla as China is one of its toughest markets considering the competition from local manufacturers like BYD. The effective execution of Tesla’s FSD in the Chinese market could be a point of differentiation that helps it claw back some market share in one of the largest markets globally. This was a large hurdle to overcome as mapping services are strictly controlled by China’s government, and so this latest development gives Tesla a leg up on the competitors which are lacking in driver assistance technologies.

- This scenario perfectly aligns with my narrative, which states that FSD will be one of Tesla’s key sales drivers and a point of differentiation among a competitive industry. It’s still too early to quantify what this could mean, but it gives me confidence in standing with my current assumptions.

Key Takeaways

- Tesla’s Dojo supercomputer will empower them to develop more powerful products

- Dojo will elevate Tesla’s Autopilot and Self-driving technology to become market-leading

- The energy storage requirements of the global energy transition will create a booming demand for Tesla’s Megapacks.

Catalysts

Tesla Dojo Elevates Tesla’s Computing Power, Enhancing Product Development In All Areas Of The Business

At face value, if you asked someone to describe Tesla, the term “auto manufacturer” would probably be one of the first things that comes to their mind. They wouldn’t be wrong, but they’ve overlooked much of Tesla’s ethos over the course of the last 10 years. Tesla could just as aptly be described as a technology company that just so happens to build cars, and Tesla’s Dojo is the perfect example of that.

Dojo is an exceptionally powerful AI supercomputer platform, custom-built by Tesla. It's so powerful, in fact, that its activation reportedly tripped the power grid in Palo Alto. Unlike its predecessor, which was based on NVIDIA GPUs, Dojo uses custom chips and infrastructure designed by Tesla, marking a significant leap in computational capabilities.

“Why move away from NVIDIA hardware?”, you may ask? Well, existing supercomputers are great at analysing an array of data and executing a breadth of tasks, but they are generally inefficient when completing one specific task. By building Dojo, Tesla can have a supercomputer at their disposal with unparalleled efficiency in executing the tasks it’s needed for.

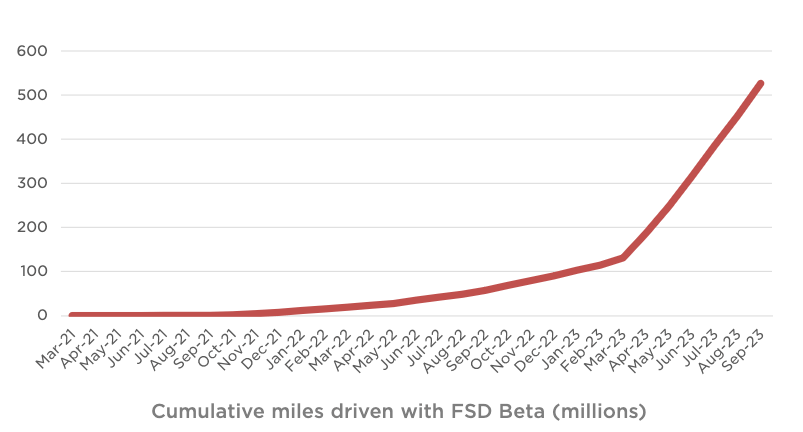

Dojo's primary role is to enhance Tesla's capacity to train neural networks using video data, which is crucial for the development of Tesla's computer vision technology and self-driving systems. Specifically, Dojo is tasked with auto-labeling training videos from Tesla's fleet and training neural networks for Tesla's self-driving system, a task that requires immense computing power

The system scales by deploying multiple ExaPODs, housing up to 1,062,000 cores and reaching 20 exaflops. This kind of scalability has never been more necessary, especially when one considers the incredible volume of data that Tesla's fleet generates. As Tesla continues to sell vehicles, this quantity of data will only multiply, and so Dojo was almost a necessary step in utilising all the data available to Tesla.

As of July, Tesla has sold 4,527,916 cars in total, and every one of these vehicles is transmitting data back to Tesla to power the company’s efforts to develop full self-driving capabilities. Meshing a huge mobile sensor and camera network with powerful edge computing capabilities to a backend supercomputer designed in-house to learn from that data is a paradigm we haven’t seen before and elevates Tesla beyond purely a vehicle manufacturer.

This system will continue paying dividends for Tesla as it’ll help propel their development of Tesla’s Autopilot and Full Self-Driving capabilites.

Tesla’s Dojo isn’t just being used for Tesla’s automotive business, with Tesla Optimus Gen 2 - Tesla’s humanoid robot - is also being developed with the assisance of computing power afforded by Dojo. Optitmus is still a fair time away from a commercial release, the Gen 2 robot only recently being demoed in late 2023, but that doesn’t mean that there’s no commercial viability, with analysts predicting demand could be as high as 10 to 20 Billion units (however, I’ll choose to ignore it for the time being when writing this narrative).

Dojo is expected to significantly boost Tesla's software and services sector. Morgan Stanley has raised its revenue estimate for this business segment to $335 billion by 2040, accounting for over 60% of Tesla's core earnings. This growth is largely driven by opportunities in third-party fleet licensing and increased average revenue per user (ARPU). Accelerating Tesla's ventures into robotaxis and software services, areas that extend beyond Tesla's core business of selling vehicles

Tesla’s Self-Driving and Automation Will Become Industry-leading Thanks To Dojo, Becoming A Valuable Sales Tool

Naturally, after discussing the merits of Dojo, the conversation turns to the merits of Tesla’s self-driving system. For those who are out of the loop on automated driving technology or struggle to see the value, self-driving systems combine the use of sensors (LiDAR, RADAR, optical etc.) and a computer to control some or all of the aspects of driving a car.

The value for consumers here is actually quite significant. At a general level, an automated driving system promises significant safety benefits by removing the human error factor in crashes. According to the US Office of Motor Vehicle Management, human error is the contributing factor behind 98% of road accidents. The motivation for delivering a reliable automated driving system is huge. If we can reduce the amount of accidents caused by human error, we can reduce the loss of life on the road and create a safer transportation system. Although this figure of 98% is quite commonly touted by automotive manufacturers, this article by The Atlantic calls this figure into question in quite an interesting read. Regardless, human inattentiveness, distraction and decision-making are key contributors to most road accidents.

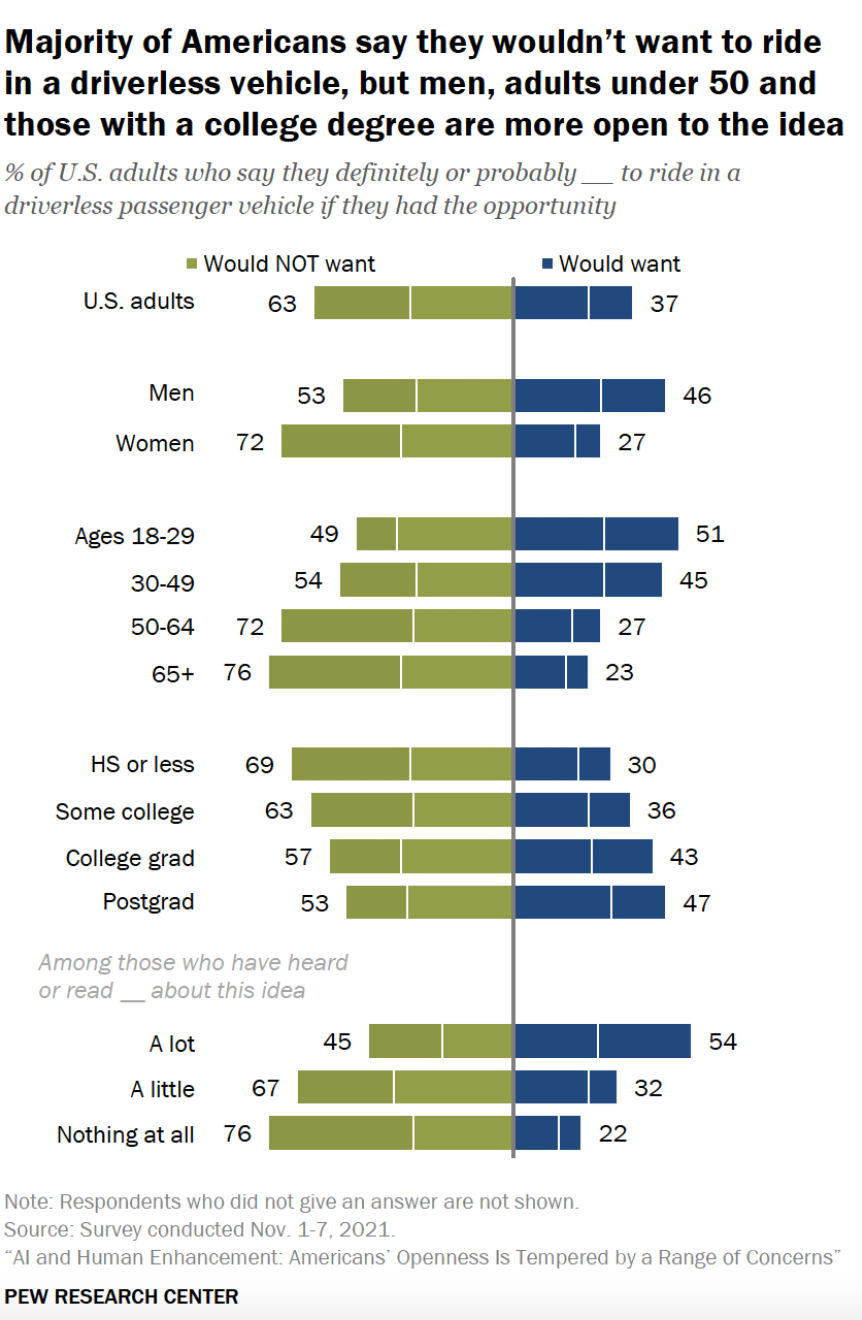

Interestingly, despite the benefits in the adoption of automated driving systems, the public still remains cautious, with 63% of respondents saying they would not want to ride in a driverless passenger vehicle if they had the opportunity, according to a survey conducted by Pew Research.

After reading this, you may ask me: “If people are so sceptical about automated vehicles, why do you think it’ll be a positive growth vector for Tesla?”. My response to that is: people are afraid of what they don’t understand. After all, Henry Ford famously said, “If I had asked people what they wanted, they would have said faster horses”.

Automated driving is the end goal of what driver assistance technology is heading towards. What may have been “high-tech” 15 years ago like parking sensors, adaptive cruise control, rear vision cameras and lane assist are now standard in most new cars. The logical step in this pattern is to continue moving towards full autonomous driving, which industry majors like Renault, Toyota, Audi, Volvo and Mercedes-Benz are already doing. What people may have seen as “too much technological intervention” back then is now commonplace. In fact, I was the same. When I was the first in the market for a car, I wanted to avoid getting a car with these technologies because I saw them as something that couldn’t be relied upon or would dull my driving ability, but my newest car has these technologies and I use them routinely, and it has made driving a much more pleasurable experience. I think the same thing will happen with automated vehicles. The population will initially fear them, then over time, it’ll be a desirable feature for all new vehicles to have.

Where I see the biggest benefit for Tesla is that they’re bringing this technology to the forefront of their automotive experience. Each Tesla model is equipped with Tesla Autopilot as standard. From there, customers can elect for Enhanced Autopilot or Full -Self-Driving (FSD) capabilities in their vehicle. By doing this, the Tesla name becomes synonymous with driver assistance technologies, and once the public opinion sways, I believe Tesla’s sales will pick up, driven by the desire to adopt autonomous vehicles.

Ultimately, I think the ability for automated vehicles to increase mobility for seniors and people with disabilities, expand transportation options for underrepresented communities, and reduce the economic toll of vehicle crashes will outweigh the fears and hesitations associated with the technology and sway public opinion in favour of pushing the technology forward.

In discussing Tesla, I must acknowledge that Tesla’s driver assistance technologies have not come without criticism. In 2021, Tesla dropped radar sensors from its Autopilot system, raising concerns over the safety of its camera-only version, Tesla Vision. This system uses eight cameras mounted around the car. Critics argue that vision-only systems may struggle in poor weather conditions, while supporters claim it reduces "noise" or confusing signals.

The automotive industry commonly uses a combination of cameras, radar, and LiDAR sensors. This way, the shortcomings of each sensor technology are addressed with another type of sensor, depending on conditions. Tesla's approach differs by relying solely on a camera-centric system, which is less expensive and scalable but considered challenging to design. Elon Musk believes the vision system has improved enough to function better without radar.

While it can be argued (in several high-profile court cases) that this is not true, I believe some of the criticism lobbied at Tesla’s solutions are unfair. As at June 2023, Tesla’s Autopilot was involved in 736 crashes, which included 17 fatalities. These figures are tragic, but this incident rate is far lower than the expected rate for unassisted drivers. Furthermore, Tesla’s incident volume may stand out above other automated driving technology, but that is simply due to the number of Tesla’s on the road far outweighing other vehicles with similar technology equipped.

Over time, with the help of Dojo, I can see Tesla’s Autopilot and FSD improving at an exponential rate, given all the Tesla vehicles on the road gathering data. I can envision a scenario where Tesla’s Autopilot and FSD technologies are the most effective and accessible on the market, acting as a huge driver in demand.

Tesla’s Megapack Will Be One Of The Key Foundations To The Energy Transition And Tesla Energy’s Growth Will Explode Because Of It

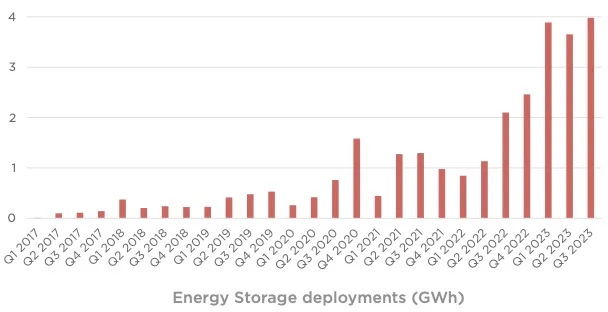

In terms of sheer revenue, Tesla Energy pales in comparison to Tesla’s automotive business, but investors may be unaware that Tesla Energy has become one of the company's most profitable divisions. Tesla Energy, which can be split into Tesla’s Solar business, Powerwall business and its Megapack business, are touted as the company’s bet on driving the global energy transition. Tesla’s Megapack business is doing remarkably well with battery storage deployments increasing by 90% year-over-year to 4.0 GWh in Q3 2023. This marks the highest quarterly deployment of battery storage systems to date. The growth was a result of the ramp-up of the Megafactory in Lathrop, California, which produces the Megapack battery

Despite solar installations outpacing other energy sources in the U.S., Tesla's solar business has struggled to maintain the levels of deployment that its predecessor, SolarCity, was able to achieve pre-acquisition. The latest figures paint quite a bleak picture as solar deployments slipped 48% from the previous year in Q3 2023. The overall solar deployments decreased from 67 MW in Q1 2023 to 66 MW in Q2 and further down to 49 MW in Q3. In response to this struggle, Tesla’s strategy shifted to assume the role of the supplier rather than the installer of their own solar technology.

Even with the struggles with solar, Tesla’s Energy business has gone from strength to strength as Megapack has become a critical solution for large-scale energy storage projects. With several of the world's biggest battery projects powered by Tesla Megapacks like the 300MW Victorian Big Battery near Geelong - the largest in the Southern Hemisphere - they have become the go-to option for such initiatives. To the joy of Tesla shareholders, Australia’s appetite for the battery packs continues to grow, with a massive order of Megapacks for the Melbourne Renewable Energy Hub, which will have a capacity of 600 MW/1.6 GWh, making it one of the largest battery systems in the world.

Given the need to undergo a global transition away from fossil fuels to meet Paris Agreement targets, I believe Tesla are ideally placed to play a crucial role in stabilizing the grid amid a growing uptake in renewable energy, especially in regions heavily investing in solar and wind energy. The largest issue with large-scale solar and wind generation is that supply cannot often be in equilibrium with demand. When there’s no sun or wind, supply drops to zero. If the sun's out and the wind is blowing, but usage remains low, the excess generation is wasted.

Tesla’s Megapack battery systems store energy when production from renewable sources outpaces demand, and then supply it back to the grid as needed. The success of the Tesla Big Battery in South Australia has led to widespread adoption of this technology in the country, with other large-scale projects like the Riverina and Darlington Point Energy Storage Systems also utilizing Tesla Megapacks.

If we consider that Solar and Wind energy generation are among the lowest levelised cost of electricity (LCOE) per MWh, we begin to see the value in Tesla’s Megapacks.

Solar and Wind farms are going to be relied on more heavily in the future to cut back on carbon emissions and Tesla’s technology is vital in making it a viable alternative to traditional coal energy generation plants.

Assumptions

Automotive Sector To Continue Down A Strong Growth Trajectory Thanks To Increasing Production Capacity And Autonomous Driving Demand

Tesla sold 1,438,992 electric cars in the first 10 months of 2023, which, when grossed up to an annual figure equates to roughly 1,726,790 vehicles sold over 12 months. This volume of sales has led to automotive sales revenue of $82,163M for period. This bodes well for Tesla, whose current production capacity (following recent production line upgrades) is 2,350,000 million units. This allows Tesla to ramp up current volumes 36% without the need for further expansion.

However, I think improvements to FSD capabilities will become the principle determinant of Tesla demand in the near future and will push demand far beyond this 2,350,000 figure over the next few years. Whilst other auto manufacturers have managed to catch up to Tesla’s EV production/sales numbers, with Chinese manufacturer BYD recently taking the crown from Tesla, their lack of focus or pessimism on autonomous driving technology could stall their sales growth in future years.

As the public comes round to Tesla, and as we approach a point where governments' ban the sale of internal combustion engines kick in, Tesla will continue to reap the rewards.

Teslas total automotive revenue for the first 9 months of 2023 totalled to $60,856M and by grossing this figure up to 10 months of revenue, we get 67,617M in automotive revenue for the 1,438,992 vehicles sold or $46,989 per vehicle

I assume that by 2029, Tesla’s annual sales volume will have climbed to 3,500,000 vehicles aided by the additional capacity brought on by the expansion of the Gigafactory in Berlin-Bradenburg and new Gigafactory in Mexico, which is due to begin producing vehicles in 2026. This translates to roughly $164,461M in automotive revenue alone. I understand that the average revenue per vehicle will change due to the introduction of the more expensive Cybertruck, but I assume there’ll be possible price cuts to the Model 3 to help keep this quite consistent.

Energy & Battery Storage Will Be The Fastest Growing Segment Of The Business

I believe Tesla’s Battery & Energy Storage will be the crown jewel of Tesla’s business for growth over the next 5 years. As previously discussed, many Australian large-scale battery projects have already engaged with Tesla for purchase of their Megapacks, but I believe this will continue to snowball. Goran has already highlighted in his narrative, there are several large-scale energy infrastructure overhaul projects including the $1.2T Infrastructure Investment and Jobs Act (US), the $737B Climate and Energy Provisions of the Inflation Reduction Act of 2022 (US) and the €2.018T Recovery plan for Europe that will all likely lean upon Tesla’s Megapack products to support a changing energy grid. Considering the company also estimates that the world will need 240TWh of energy storage capacity to become fully sustainable, the demand for Tesla’s Megapacks show no sign of slowing down any time soon.

Tesla’s Lathorp Megafactory in California currently has the scope to produce 10,000 Megapacks annually, with expansion ongoing to meet the 40GWh target for Lathorp capacity. Furthermore, to support the market demand for Megapacks, Tesla is preparing for construction of a second 10,000 unit per year Megafacory in Shanghai. On the balance of full output from these factories, plus another 5,000 units per year that I expect to come from expansions to the current plans, I expect Tesla to produce around 25,000 Megapacks annually. Currently, Tesla sells these packs for between $2-2.2M, but I could see the price per unit increase to around $2.5-2.7M off the back of lithium price increases. Using the above inputs, I estimate Tesla will earn $65,000M from its Megapacks alone. If I keep my assumptions for Tesla’s solar business to be relatively subdued at around $5,000M in 2029, my total forecasted revenues for Tesla’s Energy business in 2029 is $70,000M, up drastically from the $5,907 they made in the previous 12 months.

Supercharger Licensing Partnerships Will Boost Revenue In The Other & Services Segment

Tesla’s Other & Services segment revenue made through non-warranty after-sales vehicle services and parts, paid Supercharging, used vehicle sales, retail merchandise, and vehicle insurance. A comparatively smaller but not insignificant part of the overall business.

This area of the business is actually undergoing an interesting change, with it recently being announced that Ford and GM owners will get access to 15,000 Superchargers from Tesla’s network, earning Tesla a tasty licensing fee in the process. Wedbush Securities analyst Dan Ives estimated that these partnerships could generate an additional $3 billion for Tesla's services revenues by 2025. The other & Services segment has yielded $7,854M over the preceding 12 months, but I assume this will grow to $20,000M by 2029, as the licensing revenues from Tesla’s Supercharging network begin to snowball as additional partnership agreements are struck with other auto manufacturers.

Shares Outstanding Will See Minor Dilution

Over the preceding 12 months, Tesla’s shares outstanding was diluted by 0.6% through the exercise of options help by employees and option-holders. In 2023 Tesla announced it was cutting back stock-based compensation and so I can assume this trend will continue on for the next few years at least. I’m going to assume that Tesla’s shares outstanding willl increase 0.6% per annum over the next 5 years from 3,179M to 3,275M.

Price-To-Sales Is The Most Appropriate Valuation Metric

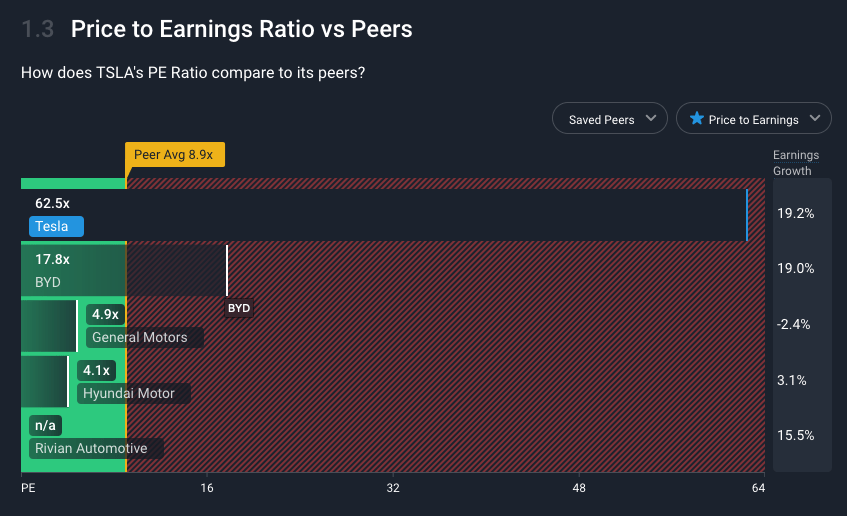

Despite Tesla having ample earnings, I am electing to value the company on a Price-to-Sales basis. Tesla’s current P/E ratio of 62.5x is quite extreme, particularly when compared to other similar peers in the automotive industry.

However, on a Price-to-Sales basis, Tesla matches more closely against the above peers, coming in at a 7x P/S ratio compared to a peer average of 1.3x.

I''m going to assume Tesla’s P/S multiple will increase slightly to 7.5x, up from 7x. I ultimately see the growth in their automotive sales and exponential growth in their energy storage business being a motivator for the market, not only keeping the valuation metrics bouyant, but pushing them further north as a market premium will be the barrier to shareholders enjoying the fruits of Tesla’s Megapack success.

Risks

Tesla’s Optical Sensors Fall Behind Competitors

One of the largest bets that Tesla made was electing to focus solely on the use of optical sensors (Tesla Vision) in their driving assistance technology. Optical sensors work well in some circumstances, however there are some significant downfalls that should be acknowledged. Unlike radar, optical sensors have a much shorter range, meaning that obstacles further away aren’t able to be detected by the system. Low-light and poor weather also inhibit optical based sensors which wouldn’t impact ultrasonic, radar or LiDAR sensors as much or in the same way.

Generally a multi-modal approach would mitigate the risks associated with any one technology, but Tesla is hedging their bets on Dojo and big data being able to deliver a more accurate service through neural network training.

If this doesn’t pan out, Tesla risks losing out on a huge sales tool for their vehicle lineup and they will struggle to meet the sales assumptions outlined in my narrative.

How well do narratives help inform your perspective?